This system is key for companies that make special items or offer unique services. Job order costing helps find mistakes before they become big problems. It makes sure every dollar gets put in the right place for each project. This system helps the shop figure out how much wood, nails, and time it takes to make each item. Not just that, it also includes the cost of keeping the lights on in the shop—the overhead costs. With practical advice and real-world examples, we’ll explore how job order costing can lead to better cost management and enhanced profitability for your business endeavors.

- By accurately tracking these key components, companies can determine the total cost of producing each product and set pricing strategies that reflect the actual cost of production.

- This includes the cost of the materials used to make the product, such as wood, metal, or plastic.

- The predetermined overhead rate is based on historical data regarding overhead costs and cost drivers such as direct labor or machine hours.

- Each decision about spending and making money gets better with good information from job order costing.

- A direct material is a physical material that constitutes an “ingredient” to make a specific product for the business.

To determine the profitability of the job

Another common mistake that manufacturing companies need to correct is incorrect record-keeping. Proper record-keeping is essential for job-order costing to work effectively. Manufacturing companies should maintain accurate records of all direct materials, direct labor, and overhead costs for each job or order. If the records are incorrect, it can lead to errors in calculating the cost of production and profitability.

Chemical Manufacturing and Consistent Costing

By working with someone experienced in this area, you can be sure that your system is set up correctly and that you are using the best practices for your business. Process costing averages costs across a high volume of homogeneous units and is suited to continuous mass production. With job order costing, contractors gain granular visibility into what each construction project actually costs to deliver.

Comparing Job Order Costing and Process Costing

At the Peterbilt factory in Denton, Texas, the company can build over \(100,000\) unique versions of their semitrucks without making the same truck twice. Job order costing is used when a unique or customized product or service is ordered. It involves assigning the costs of direct materials, direct labor, and manufacturing overhead to each specific job or order. This method is useful for companies that produce a limited number of products or services, each with different requirements. Before multiple predetermined manufacturing overhead rates can be computed, manufacturing overhead costs must be assigned to departments or processes.

c. Hitung Tarif Biaya Overhead per Unit

In addition to tracking the cost of production, job-order costing also provides valuable information for budgeting and forecasting. By tracking the cost of each job or batch, companies can identify trends in production costs and adjust their budgets accordingly. Companies can also use this information to forecast production costs and plan for future capacity needs. In job order cost production, the costs can be directly traced to the job, and the job cost sheet contains the total expenses for that job.

Technology makes it easy to track costs as small as one fastener or ounce of glue. However, if each fastener had to be requisitioned and each ounce of glue recorded, the product would take longer to make and the direct labor cost would be higher. So, while it is possible to track the cost of each individual how will legal sports betting affect your income taxes product, the additional information may not be worth the additional expense. Applying job order costing and process costing effectively depends on understanding how each method works in business scenarios. Here’s how companies use these costing methods to manage their production processes efficiently.

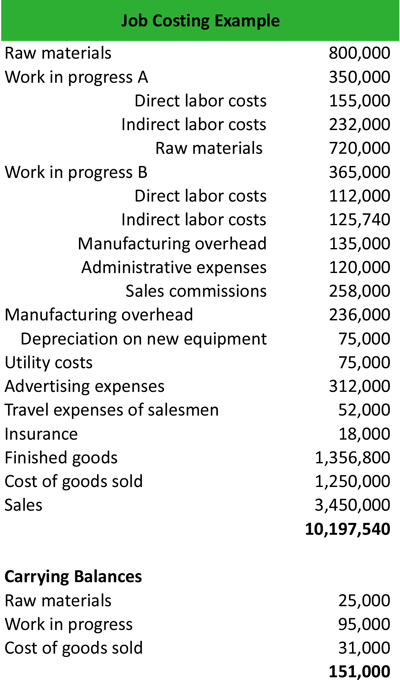

When materials are requisitioned for manufacturing, all materials are credited out of the Raw Materials inventory account. Direct materials are debited into the Work In Process inventory account and indirect materials are debited to the Manufacturing Overhead account. Use the predetermined overhead rate if you want to make your life easier, or activity-based costing if you need better accuracy. It helps the company make estimates about the value of materials, labor, and overhead that will be spent while doing that particular job. Efficient job order costing helps companies to create quotes that are low enough to be competitive but still profitable for the company. If you fail to account for your business costs accurately, then you aren’t building a firm foundation for decision-making.

The total costs for each process are divided by the number of units produced in that process during the period. Job order costing provides an accurate assessment of costs and profits across different jobs. It is one of the main job order costing examples used in specialized or custom manufacturing.